More and more investors are using the power of computing

technologies and quantitative techniques to manage their portfolios

these days. They believe that quantitative trading can help reduce the

PnL volatility resulted from emotional decision making and thus increase

the consistency of returns. However, sometimes the machine beats the

man, and sometimes it does not. Recently, quantitative funds seemed to

suffer considerable losses after British Prime Minister Theresa May

shocked markets by calling a snap election.

Among the most high-profile losers was Connecticut-based

investment firm AQR Capital Management’s $13.3 billion computer-driven

Managed Futures Strategy, which lost 1.1 percent on Tuesday, according

to an investor who was told by the hedge fund, representing a loss of

more than $130 million. The same strategy made 5.2 percent on the day

the results of Britain’s EU referendum were revealed in June. Two other hedge funds run by machines, which the investor declined to name, lost 2.8 percent and 1.9 percent. Read more

As pointed out by Maiya Keidan et al, the strategies that lost money were mostly trend-following in nature.

Trend following is a very popular strategy. Another, lesser-known

type of quantitative trading, which we write extensively about in our blog,

takes place in the volatility space. Specifically, volatility traders

and hedgers bet on the future volatility dynamics or distribution of

returns. They can do so by using mathematical models to predict the

implied and/or realized volatilities. One of the most popular volatility

prediction methods is the GARCH

model. However, there exist other lesser-known quantitative methods,

such as factor model that can be used to predict the volatility and help

with decision making. As reported by Andrea Wong, such a factor model

is being used by a hedge fund.

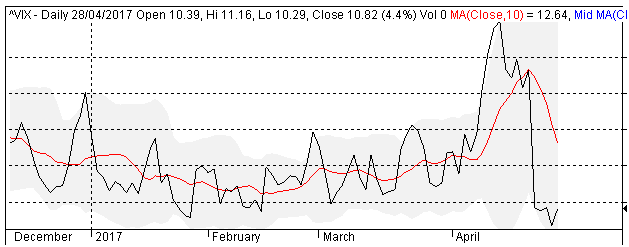

VIX as of Apr 28, 2017. Source: Yahoo financeThere are a number of reasons to heed the signals from Noorani

and his team: their model, which analyzes around 30 macroeconomic

factors from rate differentials to China’s credit default swaps,

explains 91 percent of the movement in dollar-yen over a rolling

four-month period. It sent out warning signals in mid-February before

the dollar peaked. The framework was developed by Michael Hobson, a

professor of astrophysics at the University of Cambridge. Read more

While quantitative trading is believed to be beneficial to many

market participants, some observers and regulators are worried about its

negative impact on the market, especially during a downturn. Recently

Keith Savard wrote:

The risk of turmoil is even greater given that markets already

are trying to absorb a technological revolution that includes enhanced

algorithmic trading, the proliferation of electronic bond trading

platforms and increased reliance on exchange-traded funds (ETFs).Read more

So is the jury still out whether we should embrace quantitative trading or not?

Today Rupert Hargreaves wrote that in fact many Japanese insurers are following the same strategy

According to Bank of America’s findings, the investment plans

remain largely unchanged from last year. Domestic yields are too low for

buying Japanese Government Bonds, so life insurers are having to look

overseas to acquire the yield they require.

“Insurers plan to increase their overall holdings of foreign

bonds, much as they did in the previous term, but the weighting they

give to each geographic region will greatly depend on the US rate hike

environment, European political risk, and FX trends.”

However, the big change this time around is that these companies

are planning to buy foreign bonds ex-currency hedging, which may have

major implications for US corporate bonds. Read more

Not hedging requires that you have an accurate view of the market

directions. Even if you do, it’s still beneficial to hedge. For

example, with the expectation of rising interest rates, corporate

treasurers and Chief Financial Officers started thinking about how to

hedge the interest rate risks. Recently, Ajoy Bose-Mallick et al

presented a good article on fixed income hedging. They argued that

hedging is beneficial to both sellers and buyers:

Hedging the interest rate can protect both the lender and the

borrower as it brings certainty to the interest rate costs and hence the

available cash flows from the investment. This certainty means the

borrower has one thing less to worry about on their investment. Below we

highlight the key issues that should be considered

The authors also provided some examples of hedging strategies:

Type of hedge: Interest Rate Swap, Cap, and Collar are the main

hedging instruments. The choice of hedge instruments should be aligned

to the underlying business, and prevailing market conditions. An

Interest Rate Swap fixes the interest costs and has the advantage of

known costs, however it is not flexible if the loan is to be repaid

prematurely. Fixing the interest rate also has the disadvantage of high

opportunity cost in the case where interest rates remain low or become

even lower. The Cap is an insurance-like instrument and protects the

borrowers from interest rates going above a chosen level and lets

borrowers take advantage of prevailing lower rates in case rates do not

increase. The Cap can also be unwound at no further costs in case the

borrower decides to pay the loan prematurely. However, a premium is

required to be paid for a Cap hedge. The Collar hedge is a hybrid

between an Interest Rate Swap and a Cap hedge and fixes the interest

rate costs between chosen boundaries for zero or small up-front cost. No

complicated or exotic hedges, such as callable hedges, should be

considered and hedging notionals or tenors should not exceed the

underlying loan notionals or tenor. Read more

Another, simpler, hedging technique that uses Forward Rate Agreement is presented by Sunil K Parameswaran:

Uncertainty regarding future rates of interest is a matter of

concern to both potential borrowers as well as lenders. The former would

be worried about the spectre of rising rates, while the latter would be

concerned with the possibility of a rate decline. Consequently, both

kinds of traders may wish to hedge the risk regarding future rates of

interest. One such hedging tool is a forward rate agreement (FRA).

By using such a derivative one can lock in a rate of interest for

a transaction scheduled for a future date. Forward rate agreements are

cash settled. That is, on a specified future date the profit for one

party, or equivalently, the loss for the other party would be computed. Read more

No matter what hedging strategy, simple or complex, we are using, we

should have a good understanding of the hedging instruments, market

environments, various regulatory and operational requirements.

One of the examples was Mitsui Life, a Japanese insurer who bought

foreign bonds and then proceeded to hedge the currency risks. However,

as Tomo Uetake reported yesterday, another Japanese insurer thinks that

FX hedging is too expensive and decided not to hedge:

Japan’s biggest private life insurer Nippon Life Insurance Co

[NPNLI.UL] plans to boost foreign bond holdings without currency hedging

in an effort to counter low domestic interest rates, senior company

officials said on Wednesday.

Japanese insurers have been shifting into foreign assets in

search of higher yields, but the biggest challenge has been how to

secure sufficient returns after hedging against currency swings. “When appropriate, we plan to buy foreign bonds without currency

hedging this fiscal year (to March 2018), as we expect the dollar to

strengthen gradually,” Naoki Akiyama, general manager for Nipon Life’s

investment planning, told reporters. Read more

On the other hand, as pointed out by Adriana Barrera et al., Mexican

state-owned oil company Pemex still thinks that hedging to ensure price

stability is important:

Mexican state-owned oil company Pemex will consider repeating a

recently instituted hedging program in future years, as it looks to firm

up its balance sheet and avoid the need for surprise budget cuts, a top

executive said late on Tuesday.

Petroleos Mexicanos [PEMX.UL], as the company is officially

known, reported on Tuesday that it has hedged its output through

December, the first time it has done so in 11 years, as an insurance

policy against volatile oil prices.

The oil hedging program, which will run from May to December and

guarantees a price of $42 per barrel for up to 409,000 barrels per day,

will cost the company $133.5 million. Read more

Yesterday, Tom Lee pointed out some diverging signs in the stock market:

First, Lee is concerned that the long-term yield curve has

narrowed substantially. A flattening yield curve is a widely viewed

marker of slowing economic growth, as this suggests the expected return

of long-term spending then has smaller expected return on investment.

The spread between the 30-year Treasury yields and the 10-year Treasury

yields, as Lee observed, has flattened since just after the U.S.

election in November “and historically signals market weakness ahead.”

“In the past, the bond market has been much better at ferreting

out problems and smelling slowdowns; that’s the message from the yield

curve. So I think the bond market is really taking the position that

growth is going to disappoint, and the gap between the hard data and the

soft data is still pretty big,” Lee said Monday.

10 year Treasury June future. Source: Interactivebrokers

Next, he outlined that the credit spreads of high-yield debts started widening

Specifically, Lee notes that since 1998, the market has seen 30

instances in which high-yield spreads widened 60 basis points, as it did

in late March, and the market saw a decline in 93 percent of instances

(falling by a median 4 percent). The thinking is that high-yield

indicates a tightening of financial conditions. Read more

On the same topic, Sid Verma reported on Bloomberg that there are disparities between the stock and bond markets.

In the green corner are stocks. The Standard & Poor’s 500

index is just 0.2 percent away from a record high reached in March on

bets that Donald Trump’s administration will push through tax-code

changes to spark growth. In the red corner sit U.S. government bonds,

where benchmark 10-year Treasury yields have unwound almost half of

their post-election increase, suggesting a far more pessimistic view the

economy.

“The increasing divergence between global equity market

performance and bond markets has raised questions as to whom is right,”

Jefferies Group LLC analysts led by Sean Darby wrote in a note. Read more

How long will these divergences last and what would be the final outcome?

This is the question that everybody wants an answer.

This week, Rebecca Ungarino of CNBC pointed out that the problem is

not only in the loan defaults, but also in the decline of used-car

prices:

Used-car prices are sliding, and some warn that this trend could

have sharply negative effects on both relevant stocks and on the economy

as a whole. “This is a credit bubble in autos that is very reminiscent of the

subprime mortgage crisis,” Larry McDonald, head of global macro

strategy at ACG Analytics, said Friday in an interview on CNBC’s

And the decline in the used-car prices is already reflected in the credit default swaps of auto rental companies

Avis stock price. Source: Finviz.com Bets on the failure of Hertz and Avis to repay their bonds, as

measured by five-year credit default swaps, are on the rise as used-car

prices fall and auto loan delinquencies edge higher. Elsewhere in the

industry, automakers General Motors and Fiat Chrysler this month

reported March sales figures that missed expectations; Read more

However, some experts argued that the market capitalization of the

auto industry is too small to have a significant impact on the economy.

We will see what happens next. In the meantime, and as always, risk

management is key.

Two weeks ago, in a post entitled To Hedge or Not to Hedge,

we argued that it’s always important for corporations to hedge the

commodity prices and not to speculate. This post continues with more

examples that highlight the importance of economic hedging.

As oil price fluctuates, airlines can see their revenue vary widely.

They can reduce the revenue volatility by hedging the fuel costs

Globally, risk managers quote Southwest Airlines’ long running

(25 years) and successful corporate hedging programme, which makes up

one-third of their costs. Ryan Air remains one of the latest examples of

having hedged their exposures to the extent of 95% in 2017, having

declared price certainty as their target than low prices. Singapore

Airlines Ltd, remains another south-east Asian airline that has

currently reported to have extended its hedging horizon from the

previous 2-5 years hedging an average of 37% of its total fuel cost.

Meanwhile, Malaysian Airlines has taken a prudent approach in the

current oil price environment and has aggressively hedged 65% of their

fuel oil requirements for 2017 at about a bit north of $60/bbl. While

hedging is catching up as a healthy practice to protect the bottom lines

among airline firms globally it is yet to catch up in World’s ninth

largest civil aviation market—India, where the cost of fuel for an

airline fluctuates widely from 28% to 63% of its total operating

expense. Read more

Recently, the French election has caused some uncertainties in the

market as it was reflected in the term structure of volatility. As

reported by Laura Dew, some portfolio managers did not leave it to

chance and hedged their portfolios:

The latest hedge against potential turmoil in Europe employed by

TwentyFour is via an option position on a weaker euro versus the US

dollar. With the euro/dollar back up close to $1.08, rather than $1.05

where it has recently been, even a more market friendly French election

outcome may not cost money if the US dollar finds some of its prior

inertia. There is no such thing as a free option, but we think this is a

cheap way of protecting some downside exposure to an event that may not

be as clear cut as the polls suggest. Read more

As the results of increasing political risks in Europe, the corporate

credit spreads started widening. Japanese investors took this

opportunity to buy European bonds as an alternative to low-yielding

domestic bonds. However, they have to hedge the currency risks, as

pointed out by Hideyuki Sano:

Because they do not like exposure to foreign exchange

fluctuations, they use currency hedging on a large part of their foreign

bond investment. The hedging costs are closely tied to short-term interest rate

gaps between currencies and rises in dollar interest rates mean hedging

will become costlier for Japanese investors. On the other hand, because the euro zone’s short-term interest

rates are deep into negative territory, hedging for the euro costs

almost nothing, or sometimes even produces extra returns. Read more

The above examples provided insights into large corporation hedging programs and clearly demonstrated the importance of hedging.

This week, Rupert Hargreaves of Valuewalk pointed out that the

defaults in the auto sector started to spread out to other areas of the

market:

“Will rising consumer default rates spread from autos to other

loans? Yes. We are already seeing evidence that subprime personal

unsecured and credit card delinquency rates are rising from low levels

in recent vintages, and bank loan officer surveys validate this thesis.

Further, poor performance in auto loans is increasingly emerging not

only in subprime but also non-prime (and some prime) loans.” Read more

Likewise, on the corporate credit market side, Bob Stokes recently

wrote that European credit spreads are widening, meaning that investors

have become more fearful:

Many European bond investors are not so confident about the future. Yield spreads between investment grade bonds and lower quality

debt has been widening. This means investors in the shakier debt

perceive a greater risk of defaults, so they’re demanding a higher yield

for assuming that risk.

The bond market is behaving much as it did before previous credit

crises in 2008, 2010 and 2012. … On February 7, French 10-year notes

sank to an 18-month low, sending French spreads over German debt (top

chart) to their widest level since early 2014. Dutch and Italian spreads

(middle and lower chart) have likewise widened, recently touching

respective three-year highs. Read more

However, despite these warning signs, the equity volatility still remains relatively low. In fact, Nicholas Spiro wrote

The ability of markets to climb a “wall of worry” and turn a

blind eye to the plethora of vulnerabilities facing the global economy –

from the rapid build-up of corporate debt in China to the dangers in

exiting ultra-loose monetary policies, particularly in Europe and Japan –

seems to know no bounds. This makes it nigh impossible for economists

and investment strategists to predict with any degree of certainty the

catalysts and precise timing of the next major financial crisis

He also pointed out a reason for the subdued volatility

International investors – initially speculative ones such as

hedge funds, but more recently long-term institutional investors – have

been placing big bets on volatility remaining subdued for the

foreseeable future. These bets, known as “shorting”, or selling,

volatility in Wall Street parlance, have proven extremely profitable and

are suppressing volatility further.

Yet the more subdued the volatility, the greater the distortion

in asset prices and, once financial turmoil finally erupts, the bigger

the scope for a much more disorderly sell-off than would otherwise be

the case if investors had not been selling volatility over the past

several years.

What is clear is that the Vix has become a poor gauge of

investors’ sensitivity to the vulnerabilities and threats in the global

economy that could precipitate the next crisis. Read more

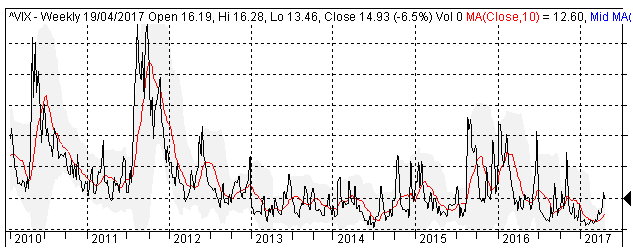

As of the close of today, the VIX index seems to be going down again.

With a decreasing VIX, investors might start thinking about selling

volatility. In fact, a post by Ellen Chang today discussed selling naked

puts. The post started with favoring put selling, but it then pointed

out some risks involved in shorting volatility:

While there is a limited upside, sellers of options should be

cautioned that there is a greater downside loss because you could lose

than more than 100% of your original capital invested. Writing options to generate higher returns comes with a large

amount of risk and “collecting an immediate payoff is not as easy as it

sounds Options writers are often compared to the house of a casino,” Ma

said. “It only makes sense if you have the large cashflow to pay out in

the short run. Remember, in the long run, the house always wins. Shorting the indexes is one strategy to profit from increased

volatility, but most investors are not comfortable doing because of the

increase in risk, said Meredith Zidek, a Hunt Valley, Md.-based options

and ETF trader. Read more

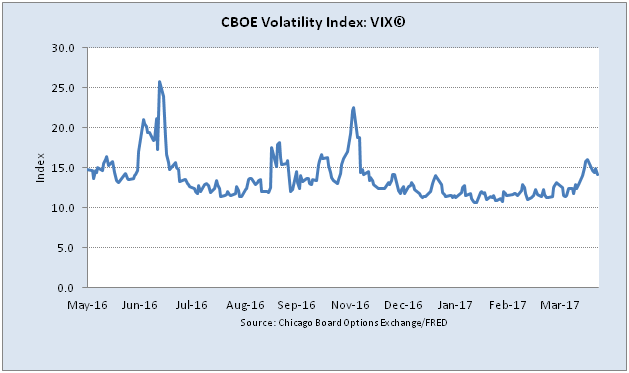

The chart below shows the VIX index from 2010 to the present.

As we can observe from the chart, the VIX has exhibited several sharp

spikes following relatively quiet periods. This means that selling

naked puts and not managing them correctly is indeed a risky business.

On the research side, a recent paper entitled Forecasting a Volatility Tsunami

by A. Thrasher presented several studies on the volatility spikes. It

also provides a method for predicting those spikes. Although we still

haven’t had any opinion yet on the merits of this prediction method, we

think the paper is worth a read

The empirical aim of this paper is motivated by the anecdotal

belief among the professional and non-professional investment community,

that a “low” reading in the CBOE Volatility Index (VIX) or large

decline alone are ample reasons to believe that volatility will spike in

the near future. While the Volatility Index can be a useful tool for

investors and traders, it is often misinterpreted and poorly used. This

paper will demonstrate that the dispersion of the Volatility Index acts

as a better predictor of its future VIX spikes.

In a previous post,

we examined the relationship between the Credit Default Swap (CDS) and

equity volatility, and argued that there is a strong correlation between

them. But like any relationship in financial markets, this one can

break down and divergence can happen.

For instance, last month we noticed that CDS in Asia and Australia

tightened considerably with respect to their US counterparts. Bloomberg

actually reported:

Credit-default swaps on the bonds of every Asian emerging market

except for South Korea have tumbled this year, outperforming debt risk

for the U.K. and for France, which has jumped amid the presidential

election campaign. Inflows into developing Asian bond markets have also

swelled in 2017 as investors bet the world’s fastest-growing region will

be able to better withstand the volatility and outflows unleashed by a

tightening Federal Reserve.

“Emerging Asia scores relatively well on both macro as well as

political stability and is likely to remain an attractive region to

invest in for the foreseeable future,” said Anders Faergemann, a senior

fund manager in London at PineBridge, which manages about $83 billion

globally. “The short-term risk is mainly associated with external

factors as the markets fear the Fed is behind the curve.” Read more

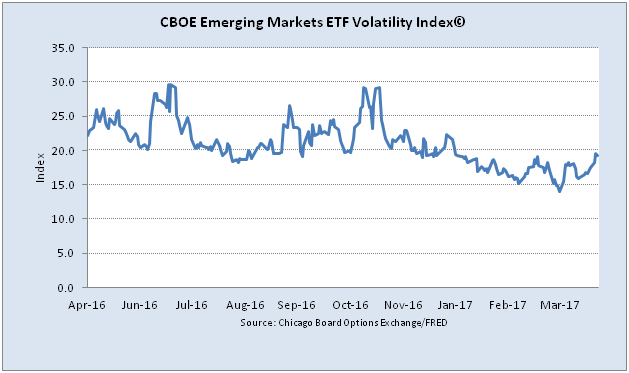

This tightening of CDS in Asia presented an interesting trade opportunity. Indeed, Asia Unhedged pointed out:

The difference between emerging market (EM) and US corporate BBB

Option-Adjusted Spread is at an all-time low. The difference between EM

volatility and VIX is around the average. This chart begs the question:

Is there a trade in shorting credit and buying equity? Read more

This means that the EM CDS is relatively low with respect to the US

counterpart when taking the volatility differential into account. The

post also suggested going long EM equity and short its CDS.

So this is an example of divergence. But it’s important to note that it happens between the VIX and CDS differentials, i.e. it represents a dislocation between secondary risks, and not primary risks.

A convertible bond (or preferred share) is a hybrid security, part

debt and part equity. Its valuation is derived from both the level of

interest rates and the price of the underlying equity. Several modeling

approaches are available to value these complex hybrid securities such

as Binomial Tree, Partial Differential Equation and Monte Carlo

simulation. One of the earliest approaches was the Binomial Tree model

originally developed by Goldman Sachs [1,2] and this model allows for an

efficient implementation with high accuracy. The Binomial Tree model is

flexible enough to support the implementation of bespoke exotic

features such as redemption and conversion by the issuer, lockout

periods, conversion and retraction by the share owner etc.

In this post, we will summarize the key steps in valuing a

convertible bond using the Binomial Tree approach. Detailed description

of the method and examples are provided in references [1,2].

Generally, the value of a convertible bond with embedded features depends on:

The underlying common stock price

Volatility of the common stock

Dividend yield on the common stock

The risk free interest rate

The credit worthiness of the preferred share issuer

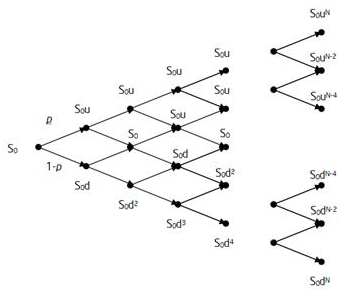

Within the binomial tree framework, the common stock price at each node is described as

where S0 is the stock price at the valuation date; u and d are the up and down jump magnitudes. The superscript j refers to the time step and i to the jump. The up and down moves are calculated as

and

where is the stock volatility, and is the time step.

The risk neutral probability of the up move, u, is

and the probability the down move is 1-p

After building a binomial tree for the common stock price, the

convertible bond price is then determined by starting at the end of the

stock price tree where the payoff is known with certainty and going

backward until the time zero (valuation date). At each node, Pj,i the value of the convertible is

where m denotes the conversion ratio.

If the bond is callable, the payoff at each node is

The payoff of a putable bond is

Here C and P are the call and put values respectively; r denotes the risk-free rate.

The above equations are the key algorithms in the binomial tree

approach. However, there are several considerations that should be

addressed due to the complexities of the derivative features

Credit spreads (credit risk) of the issuers which usually are not constant.

Interest rates can be stochastic.

Discount rate ri,j depends on the conversion probability at

each node. This is due to the fact that when the common share price is

well below the strike, the preferred share behaves like a corporate bond

and hence we need to discount with a risky curve. If the share is well

above the strike then the preferred behaves like a common stock and the

riskless curve need to be used.

The notice period: the issuer tends to call the bond if the stock

price is far enough above the conversion price such that a move below it

is unlikely during the notice period. For most accurate results, the

valuation would require a call adjustment factor. This factor is

empirical and its value could be determined by calibration to stock

historical data.

This pricing approach can be implemented in scripting languages such

as VBA and Matlab. In the next installment, we will provide a concrete

example of pricing a convertible bond. If you have a convertible bond

that you want us to use as example, send it to us.

The week ended with high implied volatilities across the board. Eric Lam et al. at Bloomberg wrote:

The calm in stocks worldwide is giving way to concern, with

investors in Europe and the U.S. rushing to hedge against declines and a

Credit Suisse Group AG index flashing a warning as the list of economic

and political obstacles grows.

There’s no shortage of potential concerns. Tensions over North

Korea’s nuclear program have intensified days after the U.S. fired

missiles at a Syrian airfield. There’s uncertainty over the outcome of

the French election, with the first round scheduled for April 23, and in

Britain doubts are emerging on whether the economy can withstand the

political shocks the Brexit negotiations will bring. Read more

So it seems that investors are very concerned with the uncertainties these days.

Interestingly, just about 10 days ago, Joe Mallen et al. of Helios

Quantitative Research presented an interesting chart that showed a

divergence between the index of economic policy uncertainty and the VIX.

The authors then concluded that most investors have become desensitized

to the news headlines:

It seems most investors over the years have simply become

desensitized to the volume of squawking news headlines. In more recent

days, despite economic policy stories that usually cause market

trepidation – such as healthcare reform (or lack thereof), the debt

ceiling debate, and short term interest rate hikes to name a few – the

US equity market has trended to very low levels of volatility. So, why

do some investors say this environment feels so volatile, but

traditional measures of volatility remain historically low? Read more

So currently are investors oversensitive?

After the French election, will we be back to the low volatility environment again?

we discussed how it’s important to hedge against a market downturn, and pointed out some strategies for doing it.

Yesterday, Brian Chappatta reported that some big portfolio managers already started buying volatility

Some of the world’s biggest bond managers have been waiting for

this moment. Rather than ponder the sustainability of the reflation

trade and its implication for yields, investors including Rick Rieder at

BlackRock Inc. and Bob Michele at J.P. Morgan Asset Management say

they’ve been betting that price swings will grow more dramatic in the

days and months ahead. That’s already borne fruit this week, with the

CBOE/CBOT index of 10-year Treasury note volatility, known by its ticker

TYVIX, jumping to the highest closing level since February. Read more

On the research side, Chrilly Donninger timely published a paper on how to protect a portfolio from a tail risk event:

Protecting an equity market portfolio with VIX-Futures eats not

only the kurtosis but also the profits of the portfolio. Being

constantly VIX-Futures long is too expensive Therefore one has to find

an appropriate timing strategy. This working paper presents a

Hidden-Markov-Model which not only has a reasonable

tail-risk-protection but even improves the overall return of the SPY.

The strategy is – at least in the historic simulation – close to what

is called in German an “eierlegende Wollmilchsau” (“egg-laying

wool-milk-sow”). Read more

In volatility space, many investors don’t know exactly what they’re betting on. Briefly, with options, they can bet on:

Terminal distribution of returns

Dynamics of the volatility

Today, we noticed an article by Alex on Valuewalk that discussed these 2 types of options trade. It concluded:

The key takeaway here is: Traders who don’t hedge delta rely on the trend of the underlying more than its volatility to profit. Traders who do hedge delta rely on the volatility of the underlying more than its trend.

It usually doesn’t make sense to hedge your delta unless you have

a professional commission structure. This is why so few do it. All

those hedging trades rack up commissions. And the execution of those

hedges requires a lot of screen time or advanced software than can do it

automatically.

So if you’re not delta hedging, a better question to ask yourself before placing an option trade is: Do I believe the underlying will trend or consolidate over the life of the option?

If your answer to that question is “I think the underlying will

trend”, you should buy optionality. The underlying will trend away from

the strike price and you’ll make money on the option you purchased.

If your answer to that question is “I think the underlying will

consolidate”, you should sell optionality. The underlying will stay

close to the strike price and you’ll collect the premium from the option

you sold. Read more

We agree with some points in the article. However, we note that:

-Even if an investor does not rehedge, i.e. he’s betting on the

terminal distribution, the volatility when he enters the trade does

matter. It’s the price that he pays for his option and it determines his

final payout.

-The article did not discuss the long term expectancy of these types

of bet which is important to know when putting on a new trade.

Last week, we noticed that

the volatility

term structure was inverted on a low reading. In fact, Crystal

Kim wrote:

Under

normal circumstances, VIX futures curve upward. It's entirely

logical -- the

longer dated futures trade at a premium to shorter-dated

futures. An inversion,

as seen yesterday, suggests that the market expects more

volatility in the

short-term than the long-term.

The

reason behind the volatility bid: upcoming elections in

France. "The April

VIX futures are bid ahead of the French elections, since they

will settle into

a 30-day VIX that captures both rounds of voting," he says.

"The U.S.

options market is finally starting to care about the French

elections."

The first round is set for April 23. If no one wins the

majority, a run-off

between the top two will take place on May 7. Read more

Vix futures term structure as of Apr 12, 2017. Source: Vixcentral.com

But these daysanomalies are

happening not just in the

volatility space. As

pointed out by

Kathleen Brooks yesterday,

the CDS market

is also acting out of sync.

On

the one hand there is a smell of caution in the air, but on

the other, capital

is not yet moving away from risky assets.

The

US corporate high yield spread should be used to time market

moves rather than

risk sentiment indicators. The US corporate high yield spread

has a significant

negative weekly correlation with the S&P 500 at -60% for

the last two

years. If this correlation is to hold, then we would expect

the S&P 500 to

continue to rally if the US corporate high yield spread

continues to narrow,

and vice versa. Read more

And finally today forex.com

observed a

breakdown in correlations

At

the start of 2017 the correlation between the S&P 500 and

the high yield

corporate spread was -53%. This seems normal as you would

expect these products

to move inversely to each other: as the S&P 500 rises,

high yield debt

falls and vice versa. However at the start of April this

correlation had

reversed to 33%, so now the S&P 500 and the high yield

debt spread move

together a third of the time. This suggests that 33% of the

time when the

S&P 500 falls, so too does the price of credit for high

risk US

corporations. Usually you would expect the opposite to occur.

Read more

Last and not least, these

articles also

gave a warning of an imminent market correction.

Yesterday the Federal Reserve Chair Janet Yellen said at a

University of Michigan event that the Fed planned to raise short-term

interest rates.

“I think we have a healthy economy now … but it’s been a long time coming,” Yellen said. Yellen said the current unemployment rate of 4.5% is “even a

little bit below” what Yellen and her other colleagues at the Fed would

consider “full employment.” She said inflation is “reasonably close” to

the Fed’s stated goal of two percent. Read more

In a previous post,

we argued that rate hikes will increase volatility through hedging of

prepayment options embedded in mortgage-backed securities.

Recently, Mark Robinson presented another argument:

Analysis from SocGen published during the fourth quarter of 2016

points to a 2.6 per cent return on 10-year notes (the equivalent rate

for the UK was 1.7 per cent). This reflects the general view that US

equity valuations are stretched based on underlying earnings. If we

accept that once investments in riskier assets such as equities are

deemed relatively expensive to government-backed debt, then stocks could

be subject to bigger price swings with increased frequency. Read more

This means that when interest rate rises, equities will appear to

be expensive relative to government-backed bonds, hence they will be

susceptible to selling, thus causing an increase in volatility.

Regardless of the argument, with a rising rate, one might think that

it’s risky to invest in fixed-income securities. However, Tim Mullaney

recently reported that:

Gundlach, CEO of DoubleLine Capital, is betting that the best way to play the coming rate hikes is by holding lots of mortgages

But how about prepayment risk?

“Gundlach doesn’t see prepayment risk as particularly high right

now, but if prepayments spike, there’s a risk of losses for the fund.” Read more

Good investment decision sometimes seems counterintuitive. And if

this is true, then prepayment risk will not be a threat to market

volatility. Let’s see how this plays out.

To add to the “against camp”, Zerohedge just published a

post, citing Eric Peters, the CIO of One River Asset Management:

“The people who are

indexing now are the same ones who were selling in 2009,” continued VICE,

agitated. “I just spoke at a conference filled for wealth advisors from all the

major players. They say the same thing - today’s buyers are not long-term

investors.” They’re guys who put $1mm into index ETFs.

“When they lose 6%-7%

and decide to sell, who will be on the other side of those trades?” And the

stocks that will be savaged worst will be the ones that lagged the indexes on

the way up. “It reminds me of 2000, when people piled into the QQQs.”

“I don’t know when the

next major crisis will hit, no one does,” admitted VICE. “But I do know that

even in the next normal correction, the market’s losses will be amplified

enormously by this move away from active management.”

Today, CNBC released another article on the same topic. This time,

the article features opposing points of view from notable researchers.

Some experts agree that the rise of ETFs has caused the volatility to

decline

“There’s no one resounding answer to [why we’ve seen] this low

volatility,” Repetto, who covers the brokers and exchanges, said Tuesday

on CNBC”s “Trading Nation.” But the growth of assets in exchange-traded

funds, which largely track indexes, “has had some impact.” Repetto pointed out that the first quarter of 2017 was the least

volatile quarter for the S&P 500 in decades — which is just one

among a host of stats showing how anomalous the lack of market movement

has been.

While some disagree:

“To a large extent, I disagree that low volatility is being

caused by ETFs,” Meziani, the author of three books about

exchange-traded funds, told CNBC in a Thursday phone interview. Read more

In previous posts, we presented 2 volatility trading strategies: one strategy is based on the volatility risk premium (VRP) and the other on the volatility term structure, or roll yield (RY). In this post we present a detailed comparison of these 2 strategies and analyze their recent performance.

The first strategy (VRP) is based on the volatility risk premium. The trading rules are as follows [1]:

Buy (or Cover) VXX if VIX index <= 5D average of 10D HV of SP500

Sell (or Short) VXX if VIX index > 5D average of 10D HV of SP500

The second strategy (RY) is based on the contango/backwardation state

of the volatility term structure. The trading rules are as follows:

Buy (or Cover) VXX if 5-Day Moving Average of VIX/VXV >=1 (i.e. backwardation)

Sell (or Short) VXX if 5-Day Moving Average of VIX/VXV < 1 (i.e. contango)

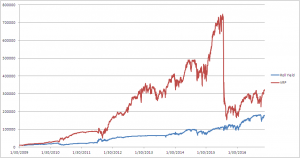

Table below presents the backtested results from January 2009 to

December 2016. The starting capital is $10000 and is fully invested in

each trade (different position sizing scheme will yield different ending

values for the portfolios. But the percentage return of each trade

remains the same)

RY

VRP

Initial capital

10000

10000

Ending capital

179297.46

323309.02

Net Profit

169297.46

313309.02

Net Profit %

1692.97%

3133.09%

Exposure %

99.47%

99.19%

Net Risk Adjusted Return %

1702.07%

3158.54%

Annual Return %

44.22%

55.43%

Risk Adjusted Return %

44.46%

55.88%

Max. system % drawdown

-50.07%

-79.47%

Number of trades trades

32

55

Winners

15 (46.88 %)

38 (69.09 %)

We observe that RY produced less trades, has a lower annualized

return, but less drawdown than VRP. The graph below depicts the

portfolio equities for the 2 strategies. Portfolio equity for the VRP and RY strategies

It is seen from the graph that VRP suffered a big loss during the

selloff of Aug 2015, while RY performed much better. In the next section

we will investigate the reasons behind the drawdown.

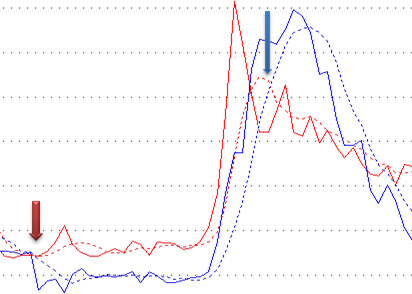

Performance during August 2015

The graph below depicts the 10-day HV of SP500 (blue solid line), its

5-day moving average (blue dashed line), the VIX index (red solid line)

and its 5-day moving average (red dashed line) during July and August

2015. As we can see, an entry signal to go short was generated on July

21 (red arrow). The trade stayed short until an exit signal was

triggered on Aug 31 (blue arrow). The system exited the trade with a

large loss. 10-day Historical Volatility and VIX

The reason why the system stayed in the trade while SP500 was going

down is that during that period, the VIX was always higher than 5D MA of

10D HV. This means that 10D HV was not a good approximate for the

actual volatility during this highly volatile period. Recall that the

expectation value of the future realized volatility is not observable.

This drawdown provides a clear example that estimating actual volatility

is not a trivial task.

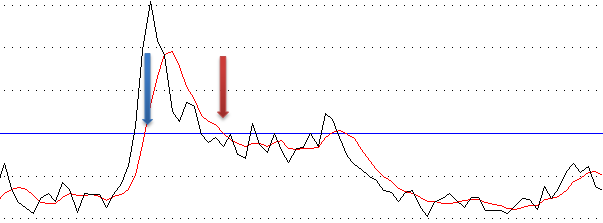

By contrast, the RY strategy was more responsive to the change in

market condition. It went long during the Aug selloff (blue arrow in the

graph below) and exited the trade with a gain. The responsiveness is

due to the fact that both VIX and VXV used to generate trading signals

are observable. The graph below shows VIX/VXV ratio (black line) and its

5D moving average (red line). VIX/VXV ratio

In summary, we prefer the RY strategy because of its responsiveness

and lower drawdown. Both variables used in this strategy are observable.

The VRP, despite being based on a good ground, suffers from a drawback

that one of its variables is not observable. To improve it, one should

come up with a better estimate for the expectation value of the future

realized volatility. This task is, however, not trivial.

References

[1] T Cooper, Easy Volatility Investing, SSRN, 2013

is the stock volatility, and

is the stock volatility, and  is the time step.

is the time step.