Last week, after the French election, the VIX plummeted and

started its journey into the low-volatility regime again. Consequently,

volatility selling strategy began gaining traction. However, FT.com

published a warning

Jim Keohane, the chief executive of the Healthcare of Ontario

Pension Plan, compares selling volatility to picking up dimes in front

of a steamroller. “You are not getting paid a lot in the current market

for the potential to get killed. That can happen very quickly,” he

warns. Read more

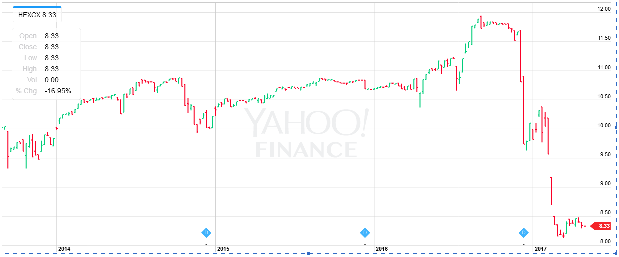

The chart below shows the price of Catalyst Hedged Future Strategy, a fund specialized in shorting volatility

Catalyst Hedged Future Strategy price as of May 2 2017. Source: Yahoo finance

As we can see from the chart, shorting volatility is indeed a game of picking up dimes in front of a steamroller, i.e. when we win, we win small, but when we lose, we lose big.

But why is volatility so low?

We provided some explanations in our previous posts

Recently, Vineer Bhansali provided more clarifications. According to him, the low volatility is due to the facts that

Realized volatility is low, resulting in a low implied volatility,

Inflow into equities is increasing,

Popularity of shorting volatility through VIX ETNs is rising,

Investors are shorting volatility through options,

Market makers and sell-side institutions are delta hedging their inventories.

Of all the reasons above, which one is the most important?

We don’t know the exact answer yet. But what we do know now is that

it’s very difficult to time the market turn, therefore it’s important to

protect our portfolios by using some inexpensive hedges. The author

also pointed out:

In most cases historically, it has paid to replace outright risk

with cheap options, or to perhaps build in some cheap downside

protection, even without knowing accurately the timing of the

correction. While it is almost impossible to time the corrections, it is

equally unwise to be superstitiously short volatility when the

dissonance between common sense and market behavior becomes so wide. Read more

No comments:

Post a Comment